Battery Storage Offtake Agreements: Swaps, Floors and Bankability Explained

A battery cannot be financed like a power station.

Revenue from generation assets is broadly linear: forecast yield multiplied by forecast power prices. That makes it straightforward to model, contract under a PPA, and present to a lender.

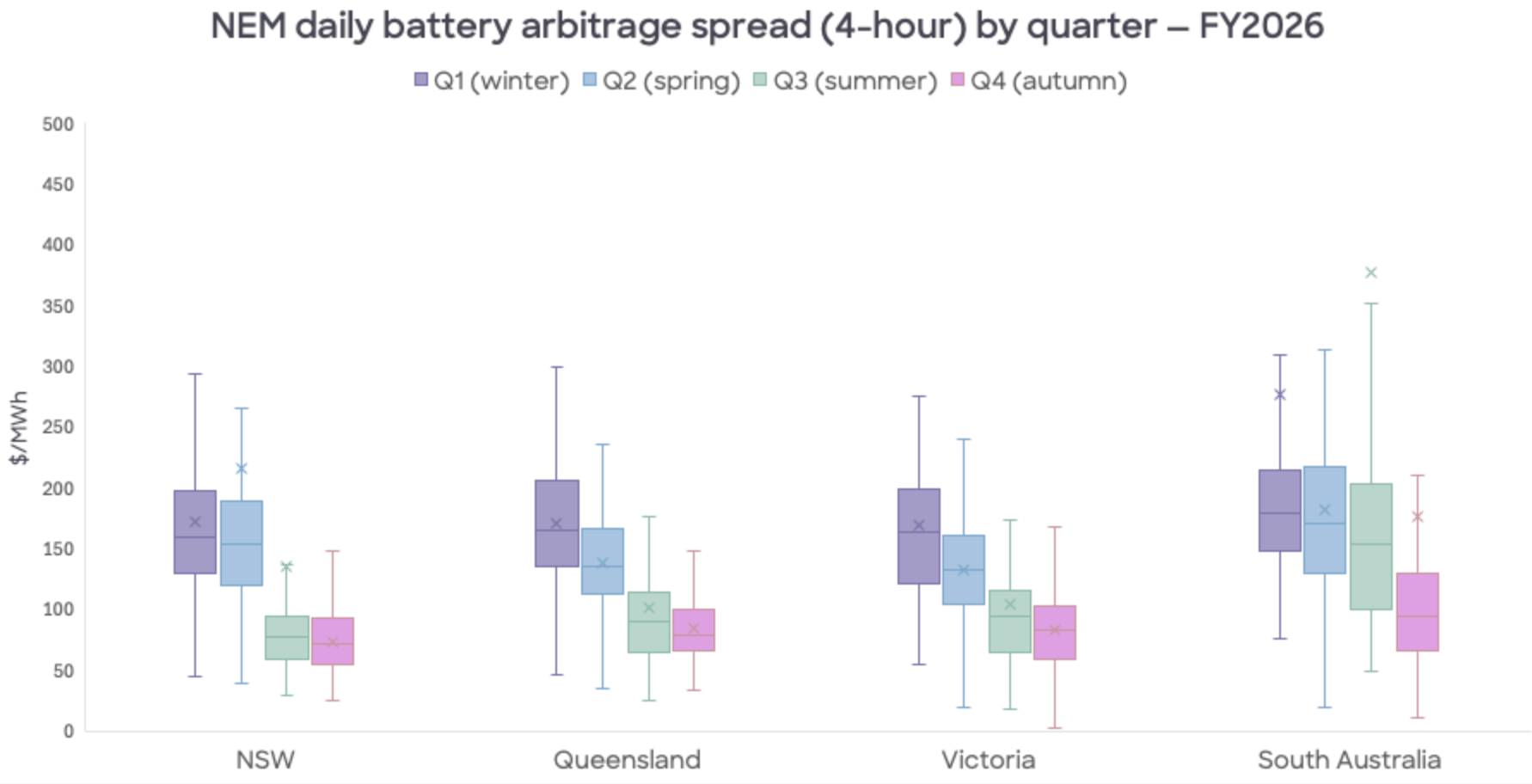

A battery however earns revenue by trading volatility across wholesale energy and ancillary markets, through algorithmic optimisation and split-second dispatch, and its income arrives in unpredictable lumps. For example, a single month in South Australia carried more than a quarter of the entire year's arbitrage value for the region.

As we discussed in our article on bankability and the funding pathway for BESS and hybrid projects, lenders will require the debt service requirements of the project to be sufficiently covered by the revenue the project will generate. The required coverage ratio (DSCR) can be lower or higher depending on how much of the project revenue is secured through contracts.

That is, to secure finance, a battery asset will need to contract some portion out — it cannot rely on favourable price volatility — because the more secure their revenue is, the lower their DSCR covenant will be and the better the debt leverage can be. Traditional contracts have been designed for coal, gas and solar stations but we are seeing new structures tailored to BESS emerging.

Standard offtake contracts are based on volume exported × spot price delivered per interval. For example a swap pays the gap between a fixed strike and the spot price, dispatch interval by dispatch interval. That works for a thermal plant or a solar farm because its value really is the price in the intervals it generates, against a volume that is mostly predictable. For a solar farm this is the typical pay-as-produced PPA: settled on, say, 80% of the asset’s generation at a fixed strike against the spot price.

A battery is different on both counts. Its value is the spread between intervals, not the price level in any one of them, and its volume is self-selected, because it decides when to charge and discharge.

The five elements of a battery storage contract

A storage contract has five main elements:

- Basis: what does it settle on? It can be based on actual physical dispatch, net revenue, or a designated shape…

- Form: a swap of cashflows, an option such as a floor, cap or collar, or a one-way capacity payment?

- Volumetric exposure: does it cover 100% of the unit's net revenue, or only a share? Does it secure a nominated capacity?

- Periodicity: is it struck every dispatch interval, or averaged over a longer window?

- Tenor: a month, a year, or the seven to fifteen years a bilateral deal needs to underwrite project debt.

No two battery offtake agreements are identical, and the right structure often depends on the specific market. That said, most contracts are rooted in one of two primary types: a swap or a put.

Swaps

Swaps for storage come in three distinct forms, depending on whether you are trading away your physical capacity, your actual revenue, or hedging against a theoretical index.

The Physical Swap / Tolling Agreement (Capacity Swap)

How it works

The offtaker essentially “rents” some of the battery’s capacity, passing on its market position and dispatch schedule to dictate how the asset is operated.

The trade-off

The asset owner gains high revenue certainty through a fixed payment in exchange for strict availability obligations; falling short can trigger penalties that far exceed the lost revenue of a standard merchant asset outage.

A toll locks current market design into the contract. If the agreement lacks provisions for shifting grid fees or rules, mid-term renegotiations can become adversarial by design: since a toll divides a fixed pot, there is no shared upside to negotiate around.

Because tolls do not adapt to evolving market outcomes, the risk increases with the tenor. This sensitivity is why tolling terms remain compressed – typically spanning four to seven years. While this duration limits overall debt sizing, the high revenue certainty makes them a powerful tool for front-loading debt early in a project’s life.

Modelling a toll must focus on how availability, degradation, and penalty exposure will impact the fixed revenue line of the project, which becomes much more complex at a portfolio level.

The Revenue Swap

How it works

This is a financial swap that settles against the battery’s actual realised net revenue (the spot revenue from discharging minus the spot cost of charging). No physical position is transferred, and the asset owner keeps control of optimising and dispatching the asset.

The trade-off

There is almost no basis risk, because the floating leg is tied to the BESS’ exact dispatch, so there is no mismatch between physical dispatch and the financial settlement of the contract.

However, because it is tied to the asset’s performance, the contract is highly bespoke, non-standardised, and requires complex verification of what was actually earned.

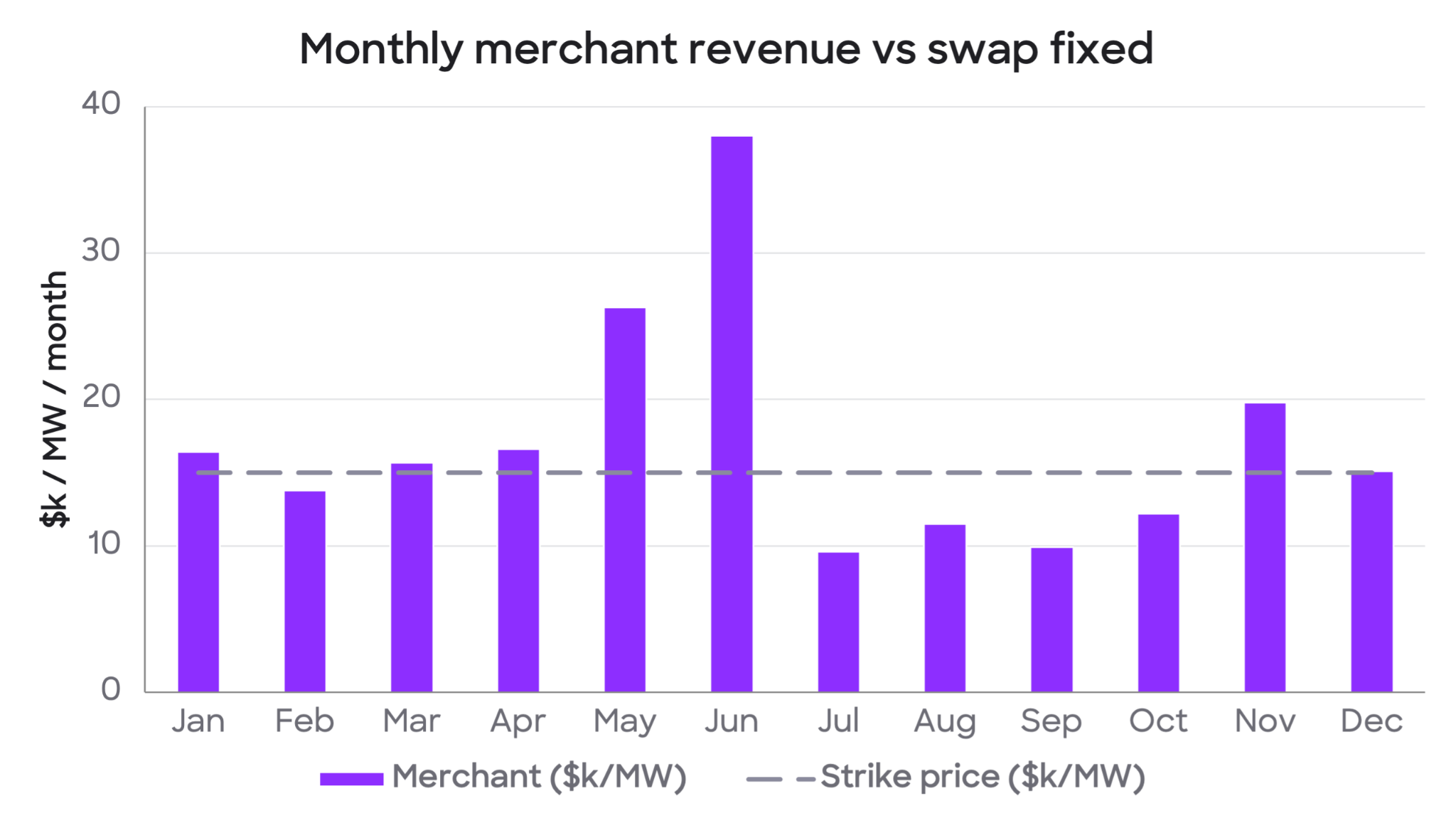

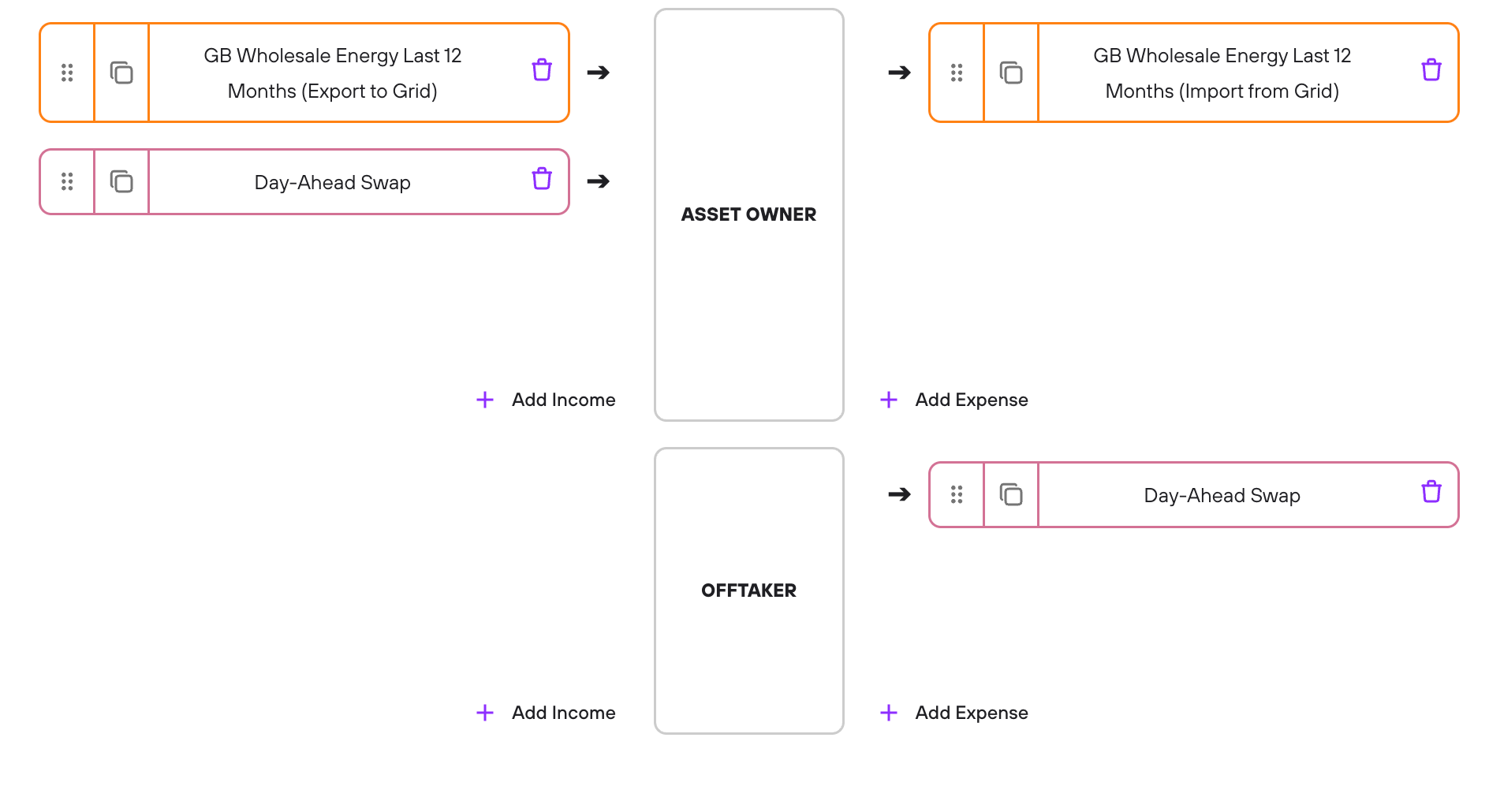

Modelling a day-ahead swap in the GB energy market using Gridcog

We modelled a variation of this structure on a GB battery site: a 100 MW, four-hour battery trading the wholesale and balancing markets, with a financial day-ahead swap on its exports.

The asset receives a fixed £100/MWh on every MWh it exports and pays away the day-ahead price on that same volume.

The floating leg here is the day-ahead price on the asset’s own exports rather than its full net revenue, but the key property is the same: it settles on what the asset actually did, so there is no index and no basis risk.

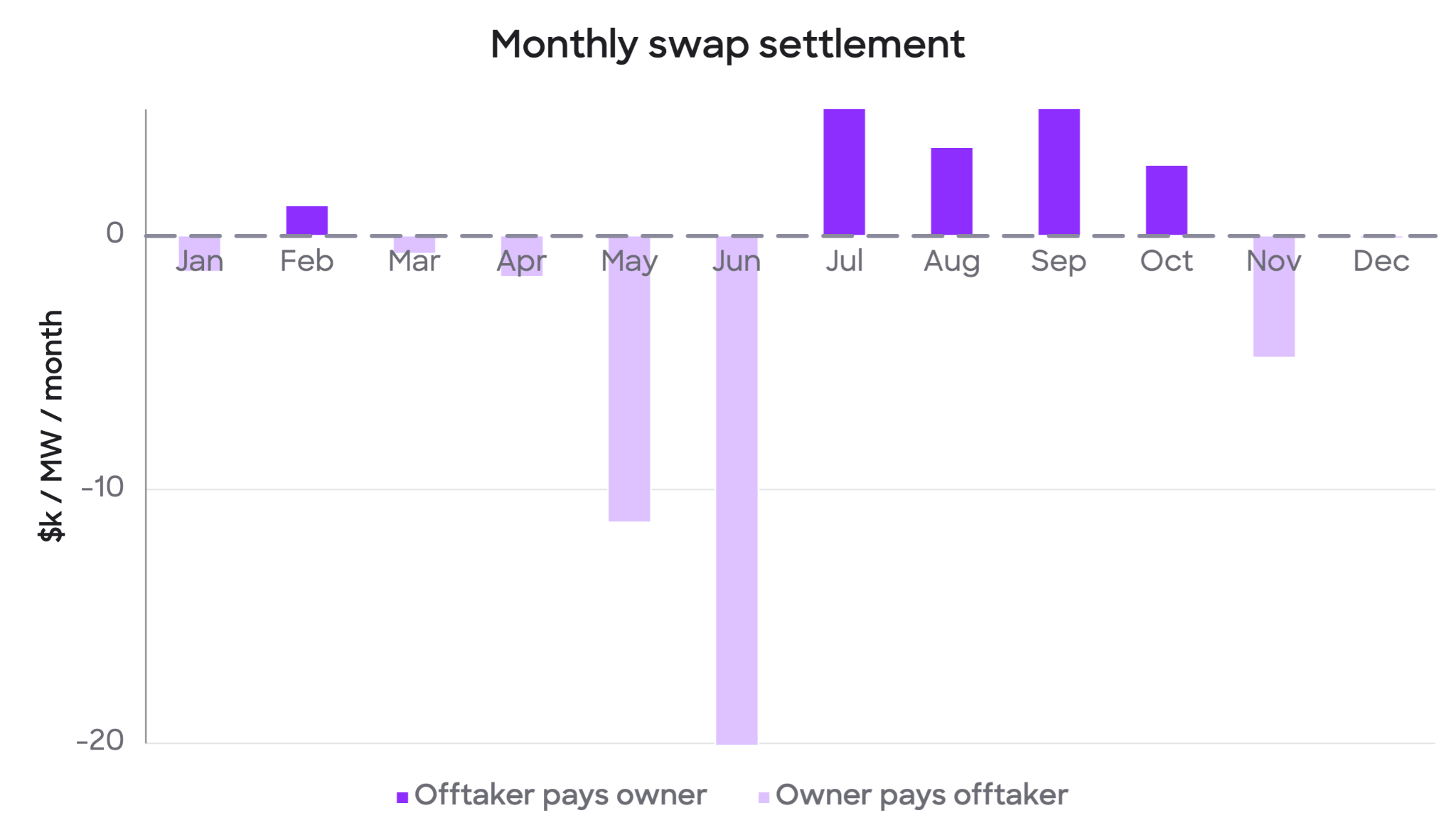

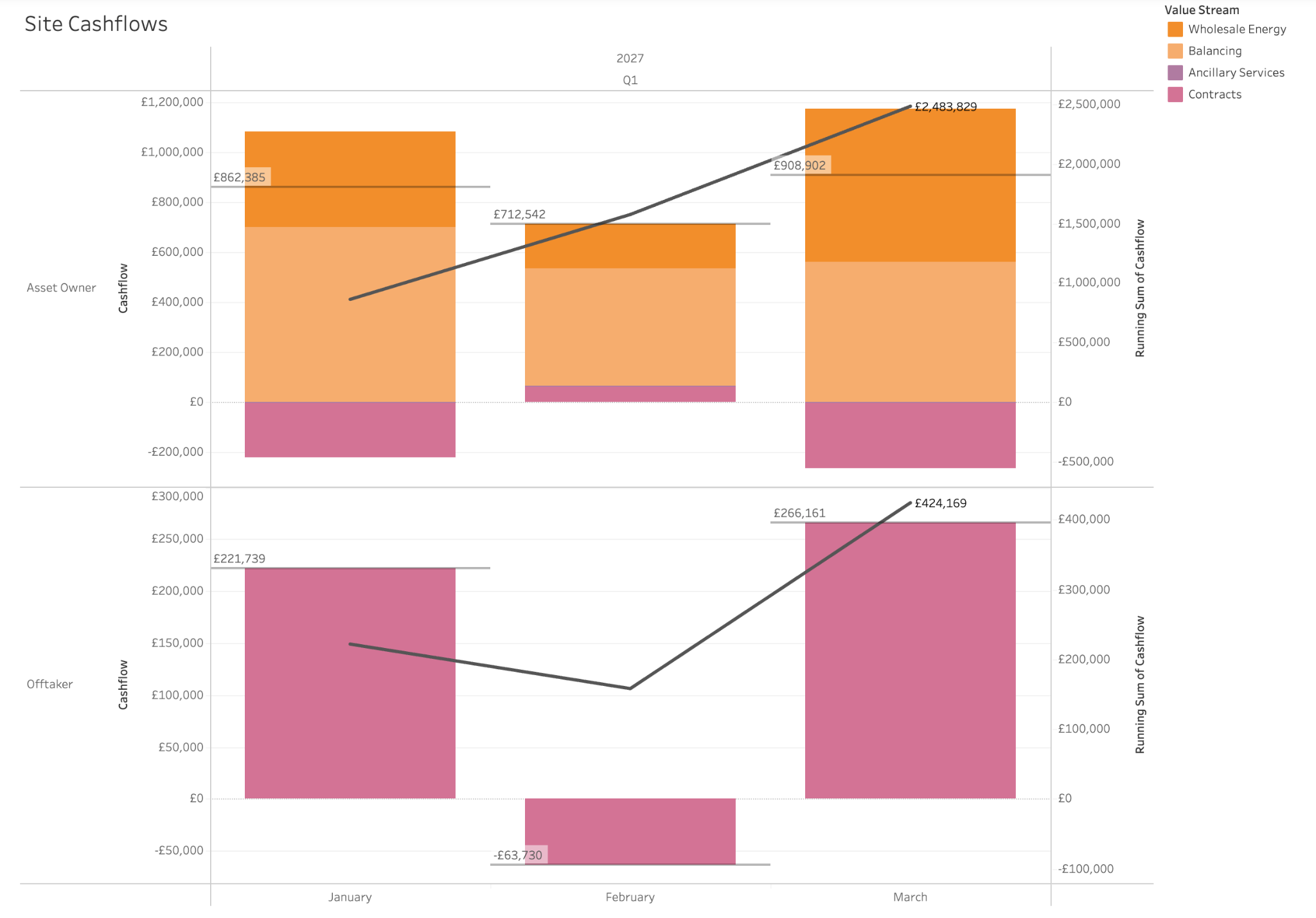

Let's look at the mechanics for the first quarter of 2027. Both asset owner and offtaker's monthly revenues are shown in the graph below.

In January, the battery's captured day-ahead price of £134.1/MWh sat above the strike, so the swap cost the asset owner £414k. In February, the capture price fell to about £87.6/MWh and the swap paid the asset £132k. In March, at £140.3/MWh, the asset handed £505k back. Every exported MWh nets exactly £100 on the day-ahead leg.

Charging costs and Balancing Mechanism revenues remain merchant-exposed, so the swap narrows total revenue from a monthly range of £13,100-£22,500/MW to £14,551-£17,304/MW.

The catch with the day-ahead swap is valuation.

Of the swaps discussed here, this is the most “hedgeable” and the one priced closest to the asset’s expected value. The challenge is knowing that value, market by market, which is a modelling problem before it is a trading one.

The Financial Swap - TBx example

How it works

A Financial Swap settles against a designated shape or index, regardless of actual asset operations. The most popular variants are the Virtual Toll, which locks in a specific battery shape, and the Top-Bottom spread (TBx, or also known as Heads and Tails).

The TBx settles against a reference index that calculates the maximum possible spread for the day. How these indexes are calculated depends on the region.

In Europe and GB that reference is usually the day-ahead auction; in the Australian NEM, which has no day-ahead auction, the index is computed on the spot market itself, but this is not mandatory. We can get creative and use other alternative indexes.

The index calculates the spread between the highest-priced and lowest-priced periods of the day, and the number in the contract dictates the cumulative hours spanned: in the TB2 example, the financial settlement will be on the spread between the average of the top 2 hours ($130+$100) and the bottom 2 hours ($5+$5) of the day. The asset owner receives a fixed $/MW contract payment and, in return, owes the offtaker the floating leg: the $110/MWh index spread multiplied by the contracted volume.

The trade-off

Like for the net revenue swap, the asset owner retains full operational control to chase intraday spikes or ancillary services. Using a benchmarked market index rather than bespoke asset data can help make the TBx appeal to a broader pool of counterparties (traders, financial institutions, utilities and corporates), increasing liquidity.

The TBx hands the basis risk to the asset owner. If the index prints a wide spread on a day the battery is offline, degraded or optimised in a different market, the owner will still owe the full index payout. This risk makes the product more suited to portfolios rather than single assets by diversifying basis risk.

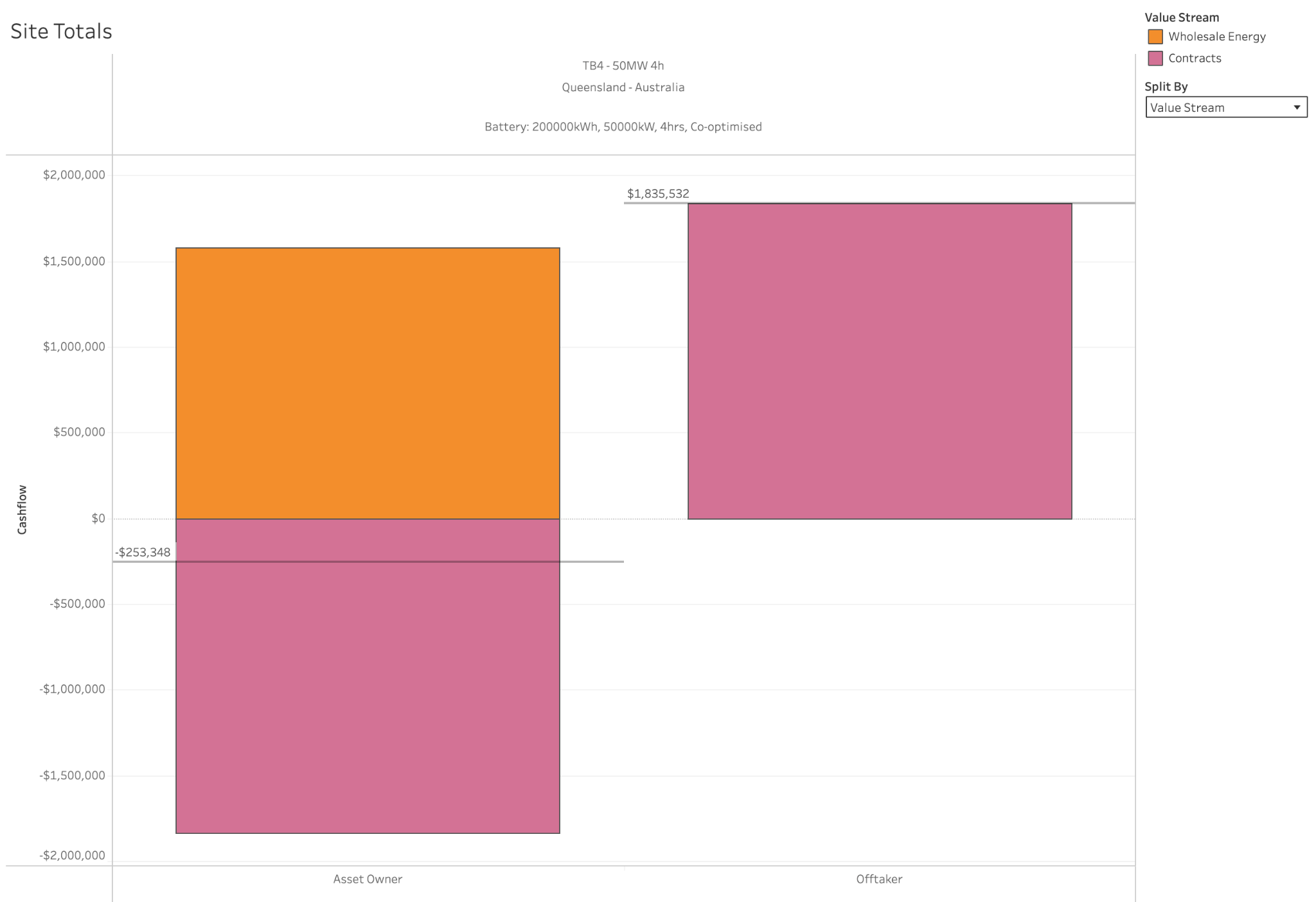

Modelling a TB4 in Queensland Australia using Gridcog

Take a 50 MW, four-hour battery on Queensland regional reference prices during the first quarter of the calendar year.

The contract is a TB4 on a nominated capacity of 50 MW: an index matched to the asset’s nameplate and duration, which on paper should make the two legs cancel. The index is computed on the same spot market the battery trades, so there is no market mismatch: what remains is pure basis risk.

In this example the TB4 spread the asset owner owes over the first quarter settles around $12,200/MW per month but the battery's own optimised net revenue comes to roughly $10,500/MW. The index outranks the asset because of a few parameters that must be well modelled before laid out in a contract:

- Perfect foresight. The index might rank each day’s hours after the fact and settle the best four against the worst four. A real battery enters the day with a price forecast, and forecasts miss: the evening spike arrives an hour late, or the cheapest charging window shifts.

- Round-trip efficiency. The nominated volume is fixed, but a battery loses roughly 10 to 15% on the round trip, so even perfect dispatch cannot earn the full index spread. Unless the contract scales the charge leg by the asset’s RTE, the owner is short that difference every day of the tenor. Same goes for depth of discharge, and battery degradation: both on usable energy, but also RTE.

- Duration mismatch. Striking a smaller sized asset against that same TB4 contract creates a gap a single asset will not be able to cover.

So why would a battery owner sign? When the terms of the contract reflect the battery’s operational constraints, the asset owner’s position holds more value streams than one market’s arbitrage: it receives the fixed payment from the offtaker, plus whatever the asset earns beyond the index, and where that edge comes from depends on the market.

In GB, the TBx settles on the day-ahead auction while the battery goes on to earn intraday, in the Balancing Mechanism and in ancillary services: properly optimised, those streams can outpace the index it owes. The NEM has a single energy arbitrage market, but the battery can capitalise on noise arbitrage, the five-minute spikes a smoothed reference price never includes, a second cycle on a multi-spike day, and FCAS stacked on top.

The foresight and efficiency gap the owner concedes, and the reference price it concedes them against, must be modelled properly, especially when the asset does not operate within a portfolio, because a single asset has no way to diversify the basis risk it wears.

Puts: floors, caps and collars

Puts are options on net revenue.

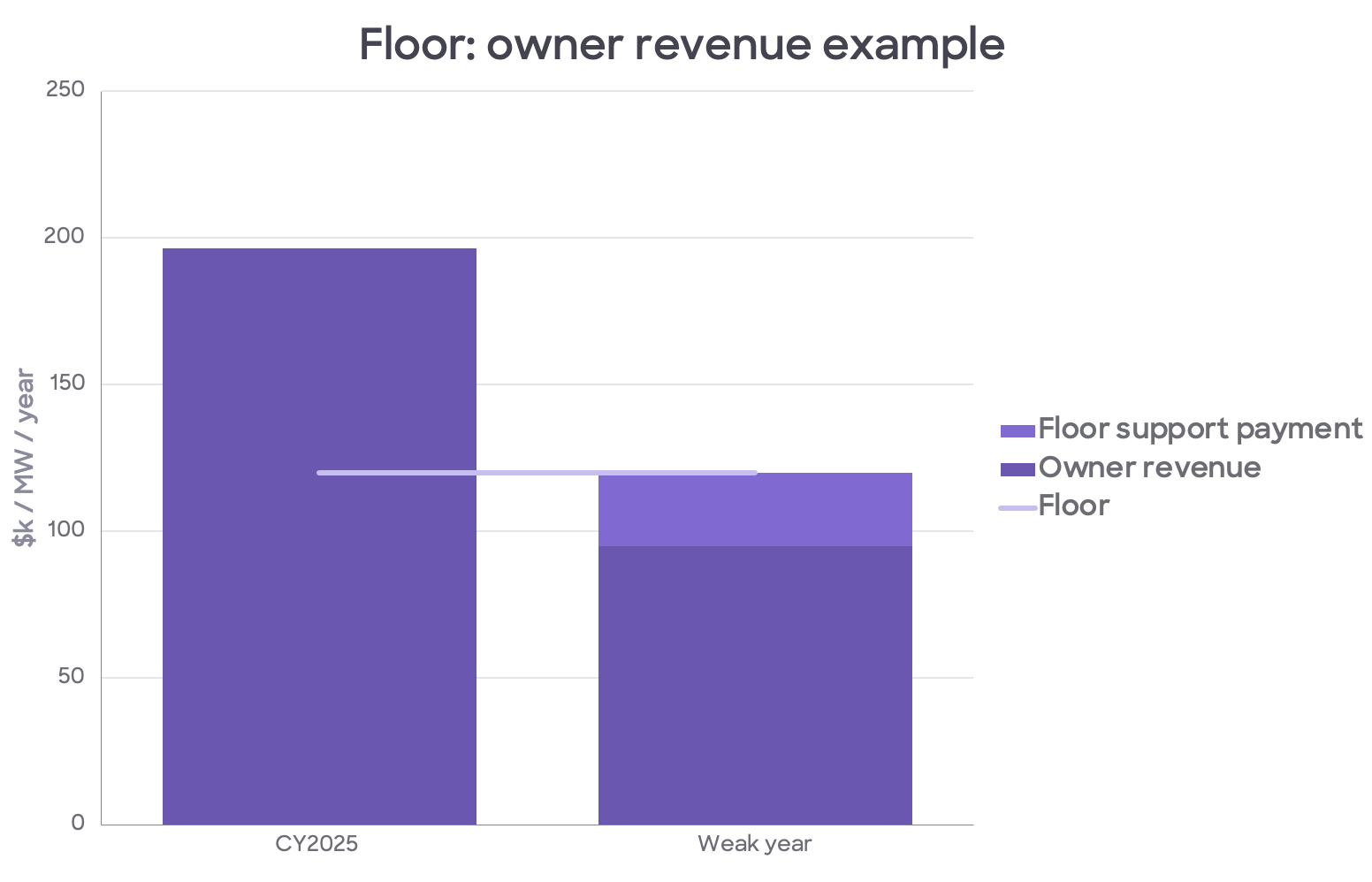

A floor guarantees a minimum: if revenues are below that floor, the counterparty will top the asset owner up. If battery revenues are above the floor, the asset owner keeps the upside, or shares it with the counterparty, depending on the arrangement. It is the most common bankability backstop for merchant storage, and can typically support up to fifteen-year tenors.

The floor exists mostly for the benefit of debt, but it can support conservative equity too. While protecting minimum revenue, the floor does not buy revenue certainty: the upside remains a question mark, which brings the expected value of the battery asset below what a swap can lock in.

A collar adds a cap to the floor, often to fund it. This will place revenue in a known band.

The trade-off

Tightening the band too far builds a revenue swap: a higher floor supports more debt but gives away upside.

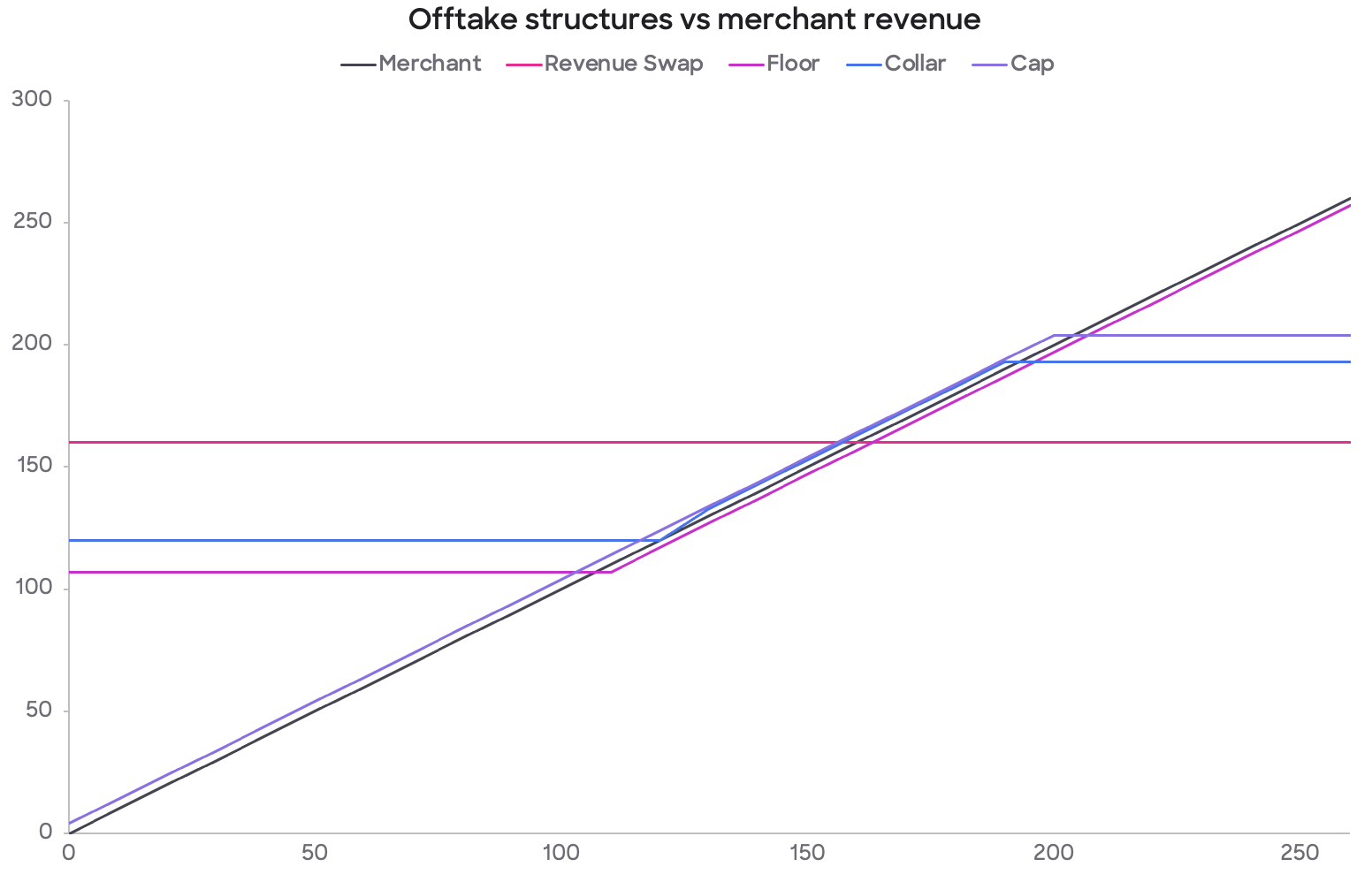

The graph above shows the revenue difference a battery can capture based on the offtakes structures it negotiates. The diagonal represents revenues of a merchant battery: the battery keeps whatever the market pays. Each contract bends that line. A swap fixes revenue flat, a floor protects the downside (while keeping most upside), a cap sells the peaks (for a premium), and a collar boxes revenue into a band.

How much upside to sell, which risks to take back, and through which structure, are questions to model thoroughly before entering negotiations.

Frequently asked questions

What is a battery tolling agreement?

A tolling agreement, also called a physical swap or capacity swap, is a contract where the offtaker rents a share of a battery's capacity and dictates its dispatch schedule. In exchange, the asset owner receives a fixed payment with high revenue certainty, subject to strict availability obligations.

What is a TBx contract for battery storage?

A TBx, or top-bottom spread contract, settles against a reference index that calculates the spread between the highest-priced and lowest-priced hours of the day. The asset owner receives a fixed payment and owes the offtaker the floating index spread, regardless of how the battery actually performed.

How long can a battery offtake floor last?

A floor is typically the most durable structure for merchant storage bankability, supporting tenors of up to fifteen years, compared with the four to seven years typical of tolling agreements.

Why can't batteries use the same contracts as solar or gas plants?

Standard offtake contracts settle on volume exported multiplied by the spot price in each interval, which suits assets with predictable output. A battery's value comes from the spread between intervals rather than the price in any single one, and its volume is self-selected because it chooses when to charge and discharge.

In closing

Battery offtake is not about finding a single or best “bankable” contract type and applying it everywhere. Each structure moves risk between the asset owner, lender and offtaker in a different way.

A toll maximises certainty but limits upside and flexibility. A net revenue swap tracks the asset closely but is bespoke and harder to standardise. A top-bottom spread can be more liquid and tradable, but shifts basis risk back to the owner. A floor protects the debt case, while leaving the upside unresolved.

The right answer depends on the market, the asset, the portfolio and the financing objective. What matters is not just the headline price, but what is being conceded to earn it: operational control, upside, basis risk, availability risk, degradation risk, or future optionality.

That makes battery offtake a modelling problem before it is a contracting problem, which is why it’s something we’re passionate about here at Gridcog.

Before a project can decide how much merchant exposure to retain, how much downside to hedge, and what price is fair, it needs to understand how the asset actually earns value across markets, intervals and operating constraints. Without that, the contract may look good on paper while quietly giving away the economics that made the battery worth building in the first place.

Want to model your own offtake scenarios? Book a Gridcog demo to see how swaps, floors and collars would perform against your project's actual dispatch profile.