Understanding P415: What it is, who it’s for, and how to participate

The P415 code modification went live in the GB electricity market on 17 November 2024, marking a significant change in how behind-the-meter flexible assets can be optimised in wholesale energy markets. Six months on, asset owners and aggregators have begun engaging with the new framework.

This blog provides a practical overview of what P415 enables, who benefits, how to participate, and the kind of value asset owners can access. You can also watch our videos for an in-depth look at specific scenario modelling.

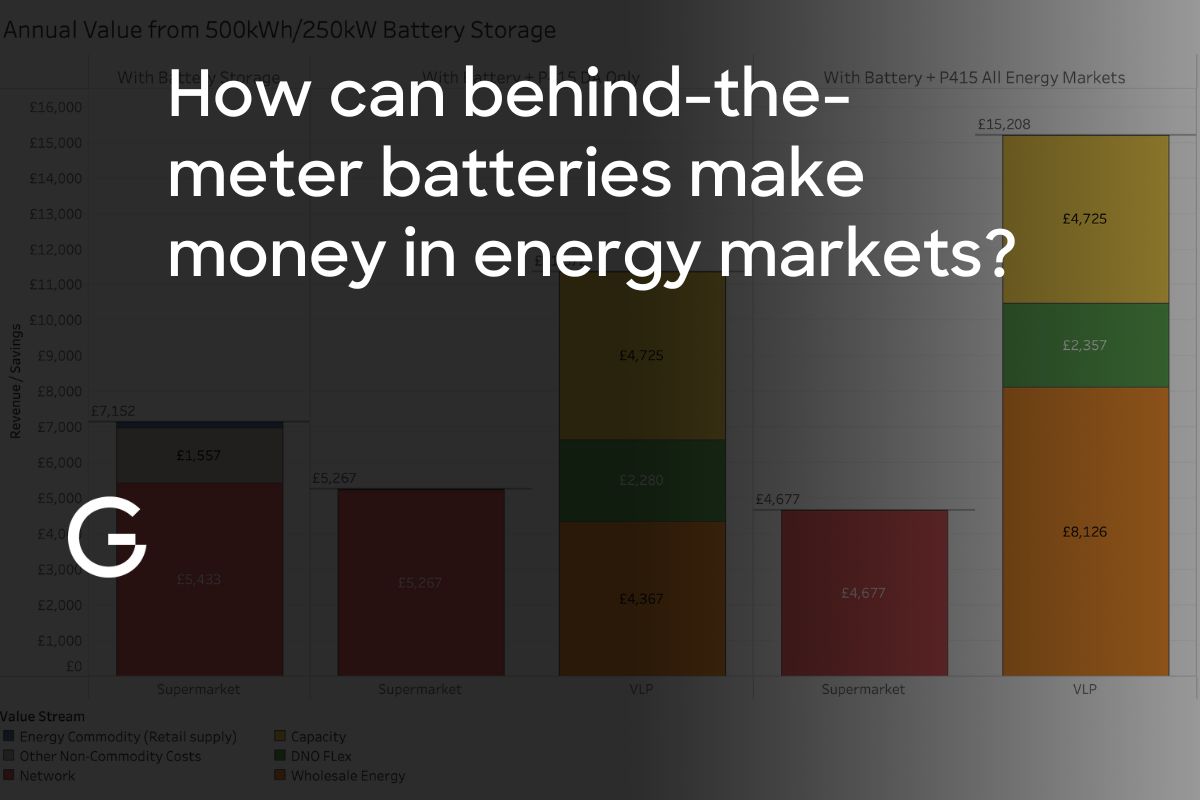

In short: P415 is a GB Balancing Code modification, live since 17 November 2024, that lets owners of behind-the-meter batteries, EV chargers, generators and heat pumps appoint an independent aggregator to trade their asset's flexibility in wholesale electricity markets, separate from their site's normal energy supplier. Gridcog modelling of a 250kW/2hr battery at a UK supermarket found P415-enabled market participation delivered materially more value than optimising for retail bill savings alone (£6,600/year), by adding revenue from Day Ahead, Intraday, Capacity Market, DSO flex and Static FFR.

What is P415?

P415 allows asset owners with flexible technologies such as batteries, EV chargers, generators and heat pumps to appoint an aggregator or optimiser to manage their assets in wholesale electricity markets. This third party can be different from the site’s energy supplier – a key structural shift.

This sits alongside frameworks introduced by earlier code changes, like P375, which enabled asset-level metering in the Balancing Mechanism. Together, these routes are creating more ways for distributed assets to support the system and access value.

Who is P415 useful for?

P415 is relevant for behind-the-meter asset owners – particularly those with battery storage, EV fleets or flexible loads – who want access to energy markets, but whose retail supplier may not offer that route.

Since P415 went live, multiple operators have registered as Virtual Trading Parties, and more are in the pipeline. This reflects growing market interest in third-party optimisation under the new arrangements.

How do asset owners participate?

Asset owners must appoint a registered aggregator or optimiser capable of accessing wholesale markets and settling energy volumes through the appropriate BSC processes (such as the MVRN process). Depending on the configuration, asset level metering may be needed to support accurate metering and settlement.

Six months on from P415 going live, reconciliation remains a challenge. Deviation volumes and centralised allocations can leave suppliers out of pocket for imbalance positions created by optimisation. Ofgem has approved P444 to improve compensation mechanisms in the Balancing Mechanism, but this will continue to be an area of development.

What kind of results can asset owners expect?

Six months on - P415 in the market

In our latest P415 video, released at the start of June 2025, we modelled a 250kW, 2-hour battery at a supermarket in southeast England. We compared how this battery would be operated and monetised in markets that P415 unlocks, versus a more traditional scenario whereby the battery works to reduce retail supply and network charges.

In the first scenario, the battery was optimised to reduce retail supply and network charges, saving around £6,600 in supply and network charges annually. But with capital costs for a 500kWh battery around £175,000, that level of savings alone was unlikely to justify the investment.

In the second scenario, the battery was optimised via an aggregator across all of the wholesale energy markets P415 enables - including Day Ahead Hourly, Day Ahead Half-Hourly and Intraday wholesale markets alongside Capacity Market, DSO flex services, and Static FFR. Frequency markets with more complex baselining requirements were excluded as they’re less applicable to smaller behind-the-meter assets.

Our modelling demonstrated that this broader market access resulted in both avoided site costs and revenue from energy services, significantly improving the business case for the asset.

%20(1350%20x%201080%20px).jpg)

P415 is already reshaping how flexible assets participate in GB’s energy markets. For asset owners, it creates a viable pathway to unlock market revenues. For aggregators, it enables new business models built on distributed flexibility.

Check out our recent (November 2025) video on modelling renewable co-located assets:

If you want to understand how P415 could affect your site or project economics, speak to a member of the Gridcog industry team about modelling your projects in Gridcog.

.jpg)