Top 5 Trends Utility-Scale Battery Storage Developers in Germany Should Watch in 2026

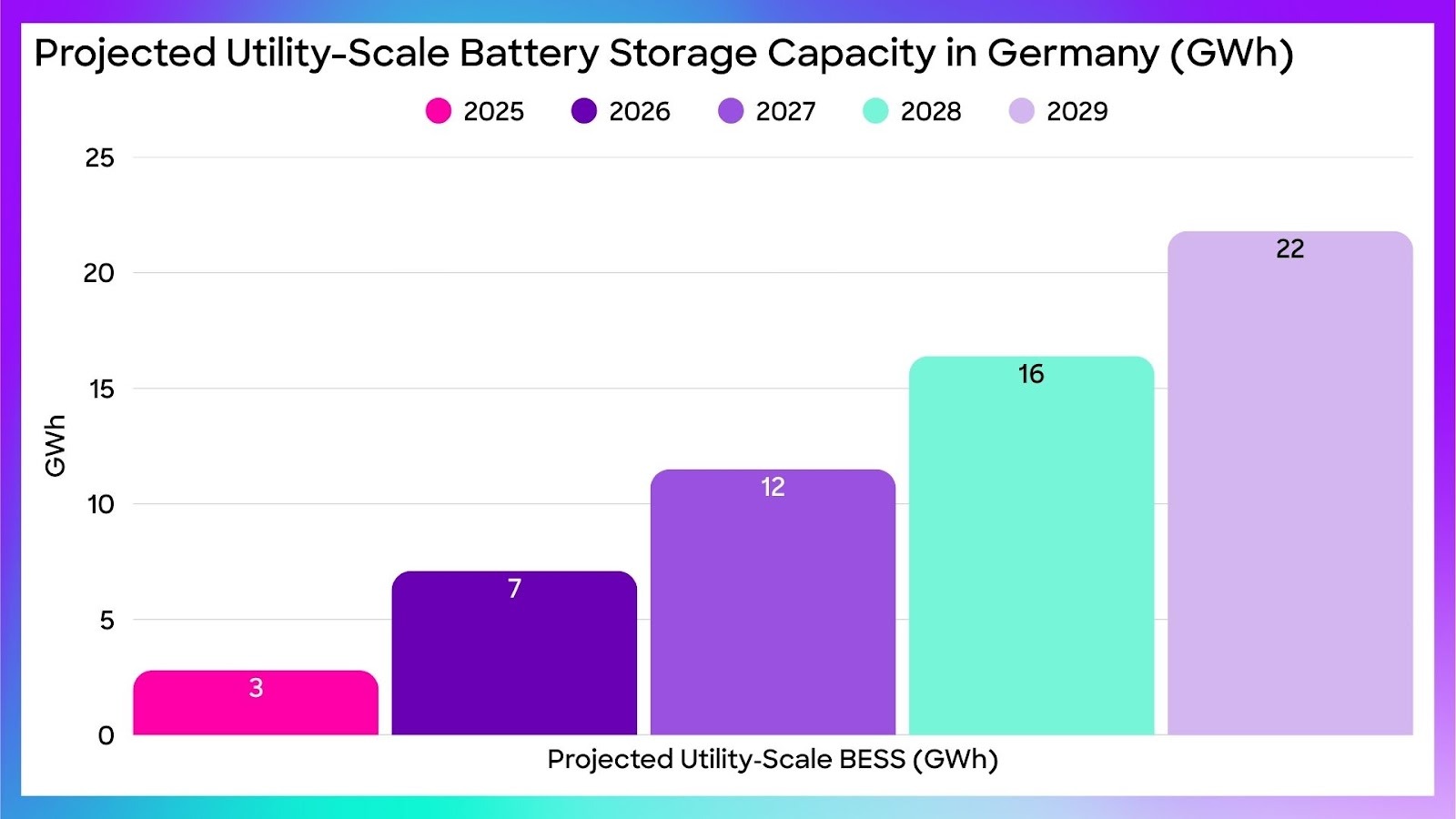

The battery storage market in Germany is growing rapidly across Europe, and Germany is one of the key drivers of this development.

At the same time, 2026 brings major regulatory and market changes that will have a significant impact on how battery storage projects are planned, financed, and operated. This article outlines the five developments that will particularly shape front-of-meter battery storage projects in the coming year.

- Privileged status for battery storage

- Grid connection challenges

- Reform of grid fees

- Updated co-location guidelines

- Additional markets for battery storage

1. Privileged status for battery storage in rural areas

With the recent amendment to §35 of the German Building Code, stationary battery storage systems above one megawatt-hour now receive privileged status in rural areas. This is an important step for battery storage project development, as permitting in these zones was previously often uncertain and lengthy.

The new regulation opens up significantly more suitable sites for utility-scale battery storage and simplifies grid access near substations and transmission lines. Under the previous law, exactly these locations were often very difficult or impossible to permit.

Since grid connection is a central challenge in the market today, this additional flexibility in site selection offers a considerable advantage.

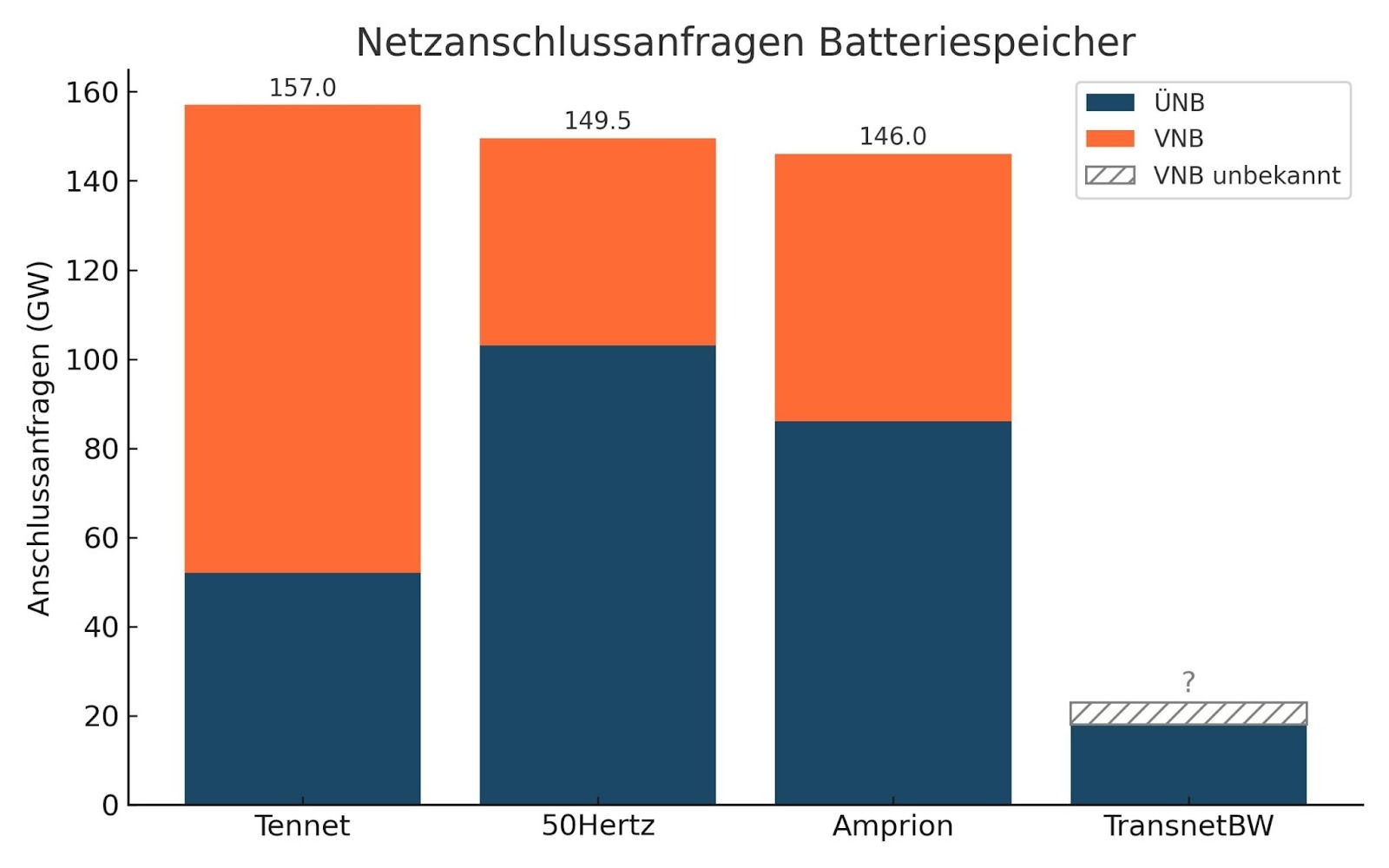

2. Grid connection: costs, capacity, and dynamic models

Despite improvements in planning law, access to the electricity grid in Germany remains the central challenge for large-scale battery storage. More than 500 gigawatts of requested projects are currently in the grid connection process, and distribution system operators are applying connection cost contributions more consistently. This makes securing a suitable grid connection point increasingly expensive and competitive.

In addition, grid operators are increasingly offering flexible or dynamic grid connection models. These can accelerate project delivery, but they require an operating mode in which the plant adjusts its output to the grid situation. For operators and investors, it is therefore important to realistically assess the technical and economic impact of these models.

In Gridcog, projects with both firm and flexible connection models can be simulated. Scenario analyses show how these variants affect dispatch profiles, cashflows, IRR, and NPV, clearly illustrating how dynamic grid contracts influence project economics.

3. Upcoming reform of grid fees for battery storage

Currently, battery storage systems in Germany are exempt from grid fees, but only until the end of 2028. From 2029 onward, the new AgNes grid fee system is expected to restructure grid fees. It is still unclear what role energy storage will play within this framework.

Project developers therefore need to consider different regulatory scenarios and design their battery storage assets so that they remain economically stable even under changed grid fee structures.

In Gridcog, different grid fee models can be tested and their impact over the entire project lifetime simulated.

4. Co-location and new requirements under MiSpeL and the EEG revision

Germany is currently working on a more flexible regulatory framework for hybrid assets and battery storage. The next EEG revision is expected to further specify the fundamental rules for hybrid systems and storage.

Building on this, MiSpeL regulates the practical implementation. It is currently in the Federal Network Agency’s determination process and is expected to define from 2026 onward how storage can use both renewable energy and grid power without violating EEG requirements. Two models are proposed: a detailed metering-based separation of EEG and grid power, and a simplified flat-rate model for smaller systems.

Through the combination of the new EEG framework and MiSpeL, developers gain significantly more flexibility. Battery storage systems will be able to switch more easily between charging with EEG power and grid power without losing support benefits.

In Gridcog, these energy flows between generation, storage, and the grid can be mapped in detail, making the economic and regulatory effects of operating under MiSpeL guidelines clearly visible.

5. New markets and additional revenue opportunities for battery storage

From 2026 onward, two new markets will open for battery storage in Germany: momentary reserve, an inertia-like product with very fast response times, and reactive power provision, which transmission system operators are increasingly tendering explicitly.

These markets offer additional revenue opportunities for battery storage projects. To participate, operators must understand the technical requirements, such as response times, control quality, and inverter behaviour

Conclusion

Overall, 2026 will be a decisive year for the German battery storage market. Our modelling platform Gridcog helps battery storage developers and investors navigate this growing complexity and accurately assess the financial impact of regulatory changes on IRR and NPV.

If you’re a front-of-metre developer in Europe and need some help understanding your options, then hit up the Gridcog team.

.jpg)