Analysing the new Octopus x BYD Dolphin V2G Scheme using Gridcog

Octopus has announced a bundle which allows customers to lease a BYD Dolphin vehicle that can charge for free at home for £300 per month.

The premise is that a customer will be able to lease the vehicle, paying a fixed monthly fee. There are some conditions though. The vehicle:

- Needs to be plugged in for a minimum of 12 hours a day on average

- Cannot use more than 210kWh of energy in a month or drive more than 625 miles.

While the vehicle will unlikely be charging (or discharging) every moment of those 12 hours, Octopus will decide when it makes economic sense to charge the vehicles based on the price signals they are exposed to; this is smart charging.

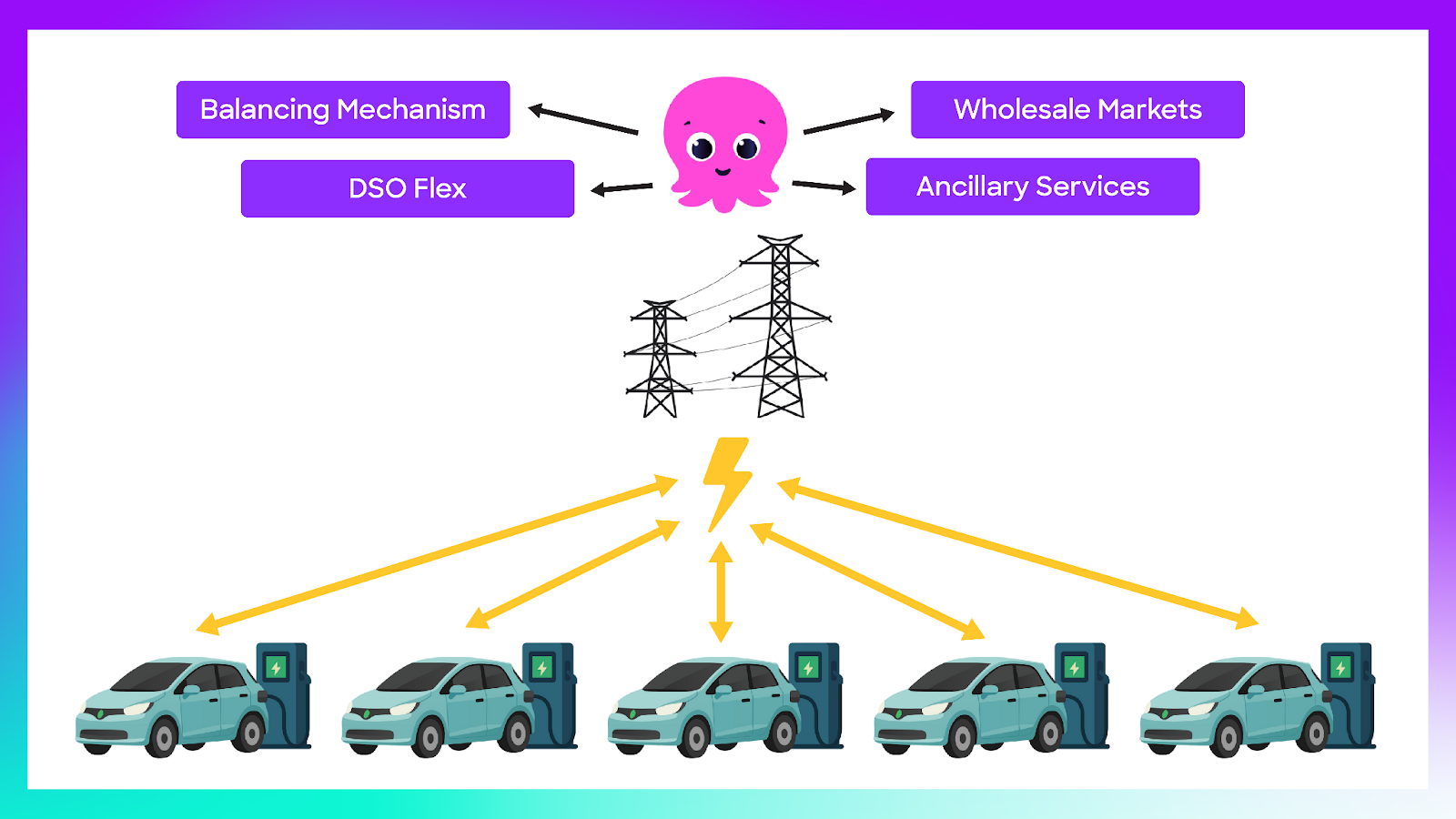

But more than just smart charging, the vehicles will also need to be enabled for Vehicle to Grid (V2G). By using the batteries as a source of flex these will be able to discharge to the grid or reduce demand during high price events. One vehicle by itself won’t be able to do much, but the vehicles will be aggregated - or grouped together - and the combined power from the vehicles will be able to offer an additional source of energy, providing flexibility to the grid, and the ability to participate in markets.

In addition to market services, having access to this flexibility acts as an option for Octopus Energy to manage risk or imbalance positions in their generation and supply portfolio much like how a battery toll contract or financial derivative can.

Modelling the scheme in Gridcog: Charging Profiles

So how does this stack up from an economic perspective? To answer this question, we ran a simplified version of the scheme for one vehicle in Gridcog. Now, of course, from a supplier (Octopus) perspective you’d be modelling far more vehicles and the level of flex behind the scenes would be more complex than what we are showing here. For example, we have not modelled financial risk saving from managing their imbalance positions. We have also not modeled the relationship between BYD and Octopus as this is not something we know the details of.

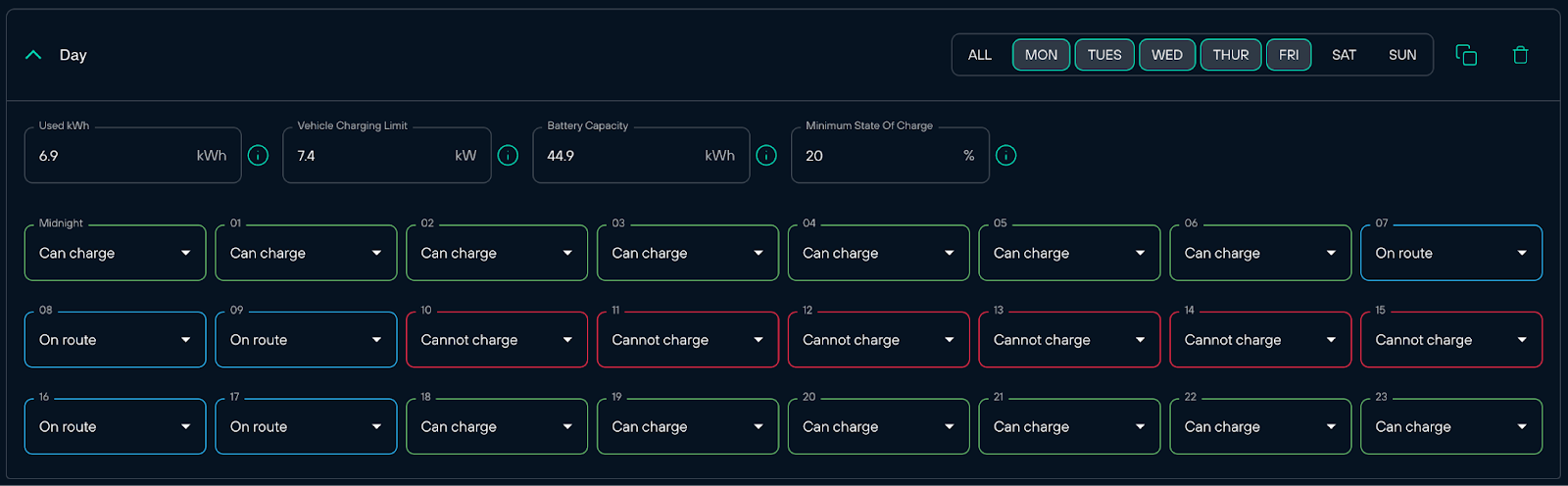

We start with creating a vehicle schedule based on typical usage patterns of the vehicle, ensuring that at least 12 hours of charging are allowed. These are shown by “Can charge” below.

The schedule shown is for weekdays, assuming the vehicle can charge overnight and is plugged in from 6pm to 7am. The weekend has a slightly different schedule, but you get the point. The “used” kWh is the energy used per day in line with the 210kWh limit per month as per the Octopus offer. The vehicle charging limit is based on how fast the vehicle can charge with the Zaptec pro charger and the battery capacity is set to what the BYD Dolphin can offer. We have set a minimum SoC to 20% of the EV so we always allow some capacity just in case. It's important to note that a vehicle’s primary purpose is to get you from A to B, not trade in energy markets. So while V2G will happen, it will only be permitted within the confines of the driving patterns of the user.

Modelling the scheme in Gridcog: Market Exposure

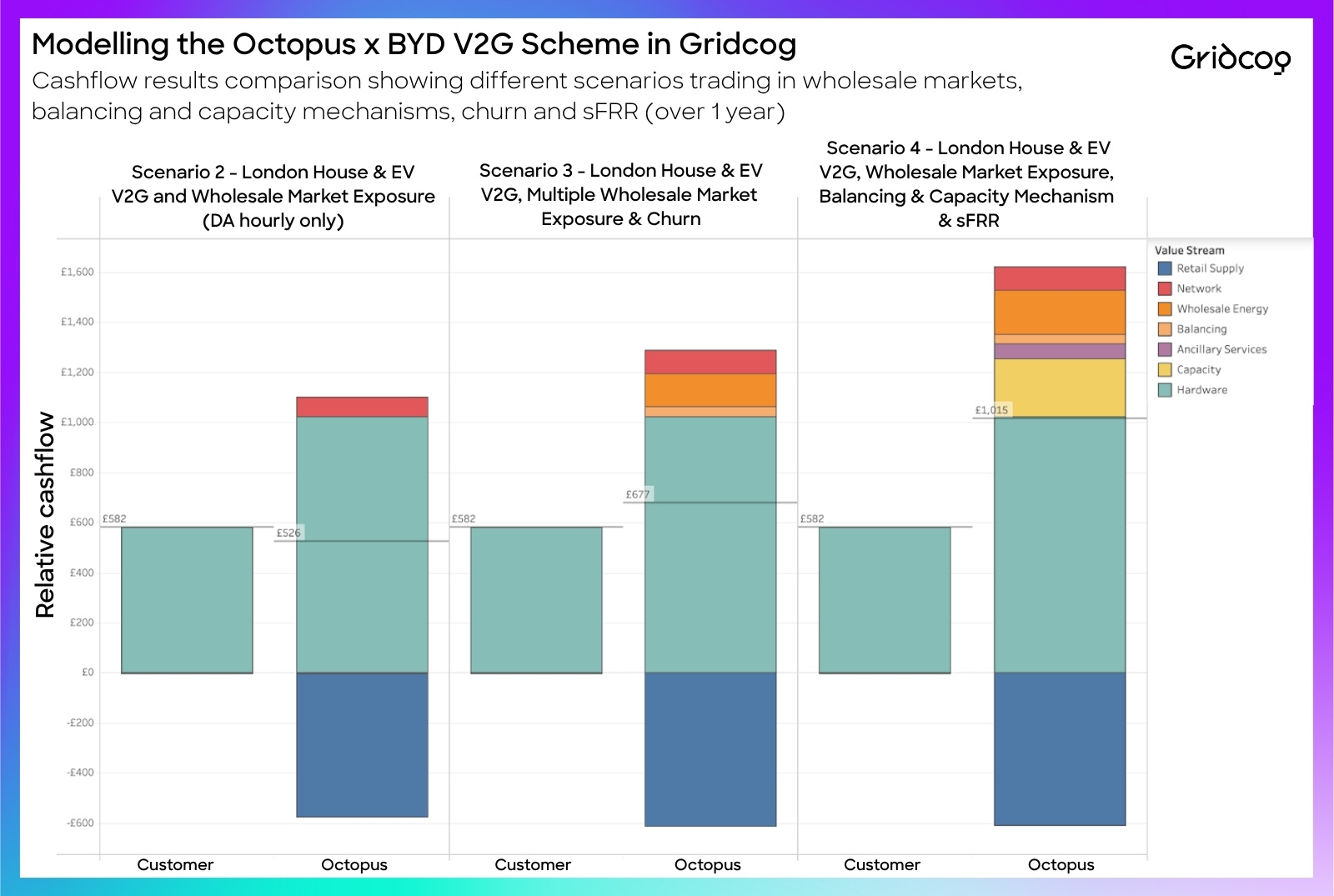

After creating the above schedule, we’ll look at how a vehicle may behave and the economic outcomes with varying degrees of market exposure. We will run the project for one year from July 2024 to June 2025 with the following scenarios:

- Baseline scenario - a customer paying a residential price cap tariff for home electricity usage, leasing a petrol equivalent to the BYD Dolphin and vehicle fuel costs.

- Electric vehicle with Octopus Power Pack Offer buying and selling on the Day Ahead Hourly market. The customer continues to pay the residential price cap tariff for home electricity consumption.

- Electric Vehicle with Octopus Power Pack Offer trading on the DA hourly, DA half hourly market, intraday continuous market, enabling churn (trading between markets when more than £20/MWh can be made). The customer continues to pay the residential price cap tariff for home electricity consumption.

- Electric Vehicle with Octopus Power Pack Offer trading in the above three markets, exposed to the Balancing Mechanism, Capacity Market and Static Firm Frequency Response (sFFR). The customer continues to pay the residential price cap tariff for home electricity consumption.

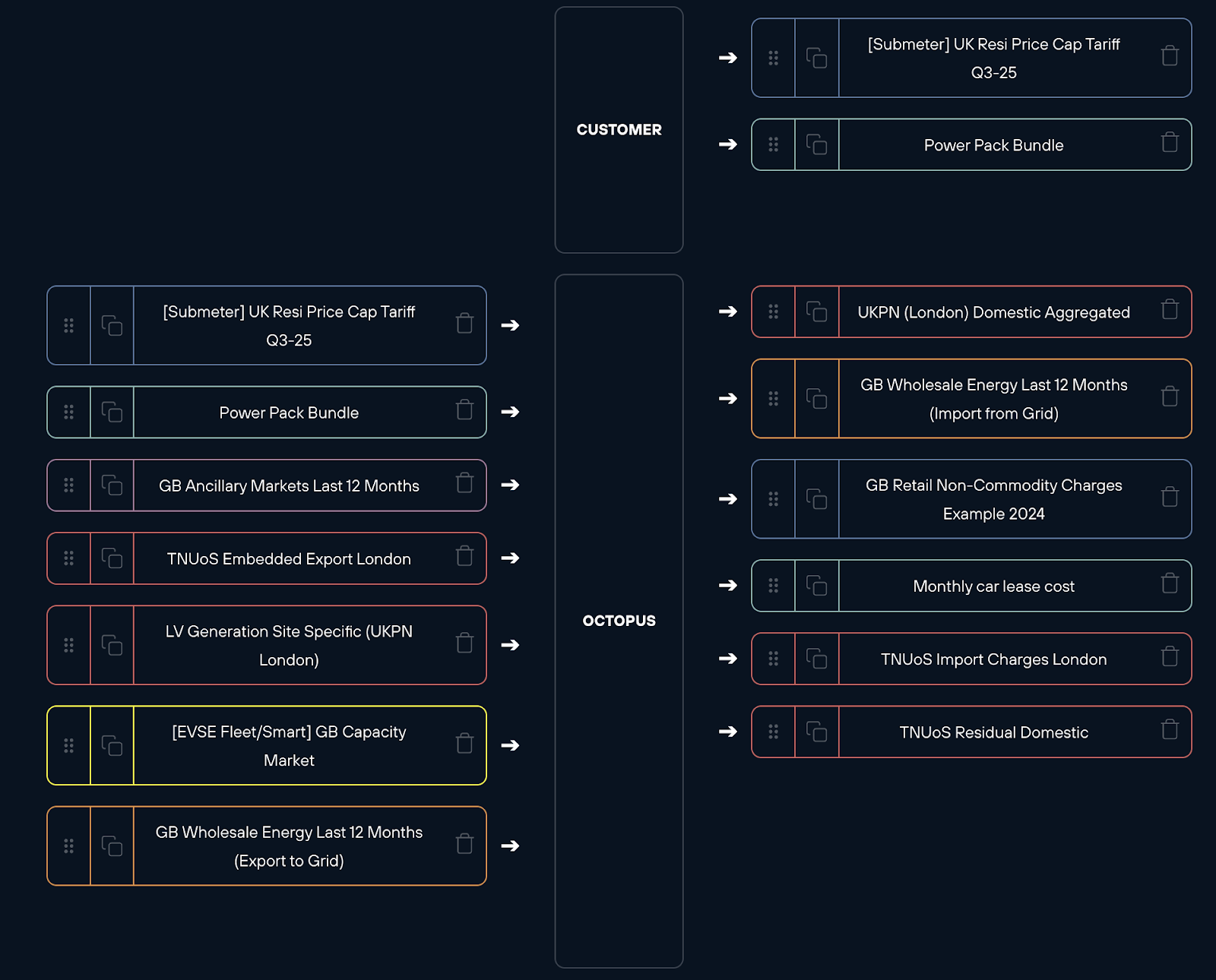

Here is a snapshot of the Commercial Model of Scenario 4:

Analysing the Results

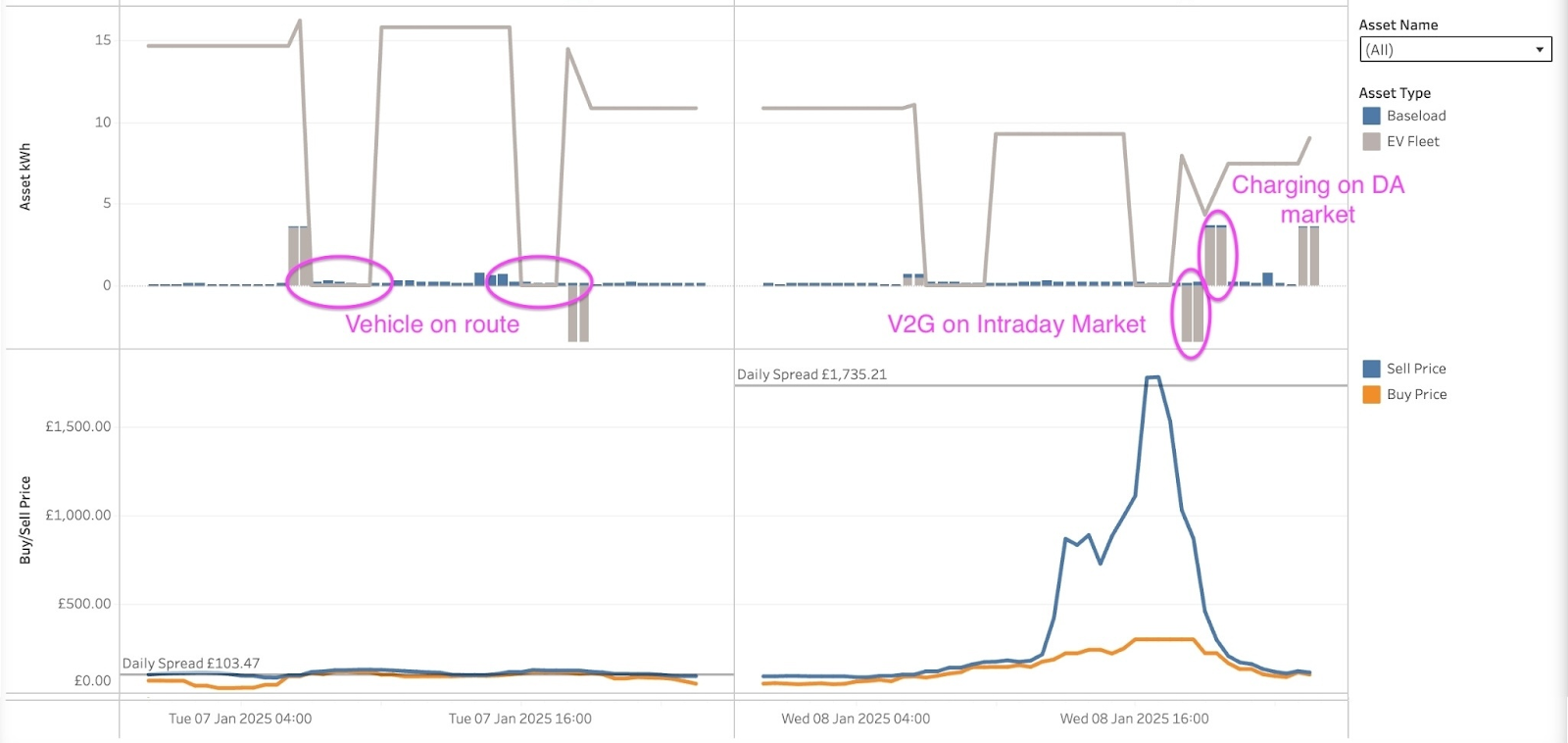

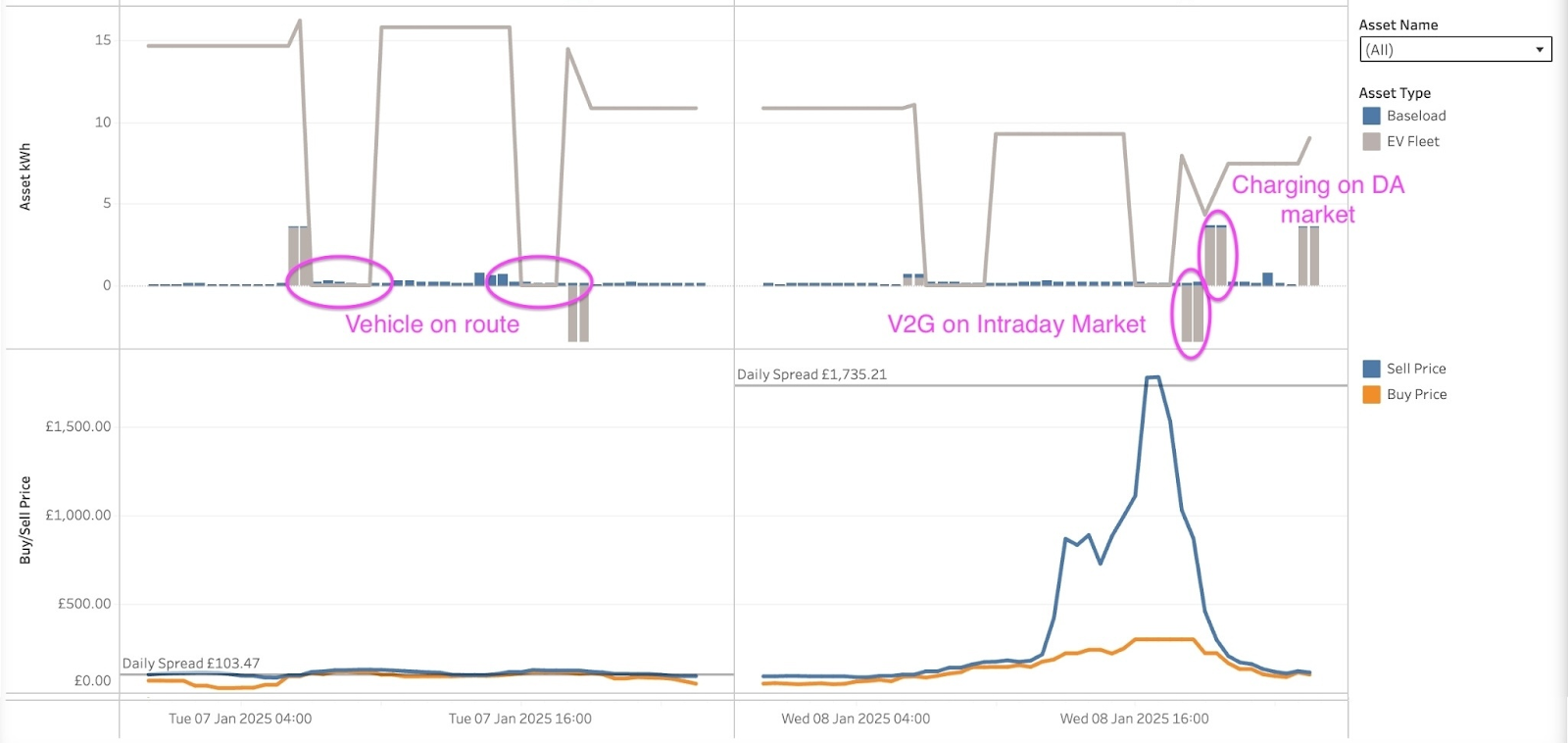

So let’s take a look at the results. First let’s have a look at some V2G behaviour that Octopus may try an optimise for. Below is a day that was dictated by trading between wholesale markets. We’ll look at the 7th and 8th of January 2025 as two contrasting examples of wholesale price spread when a vehicle is exposed to three wholesale markets (DA hourly, DA Half hourly, Intraday Continuous Auction). On the 7th of January 2025 there was a relatively low price spread of of £103.47/MWh and 8th of January 2025 having a spread of £1,735.21.

On the 7th of January with a low spread, EV available SOC was dictated by the EV driving patterns and did not involve wholesale energy trading. Compare that to the 8th of January where the vehicle actively tries to charge and discharge as fast as the charger permits to charge on the DA market and discharge to the intraday market to capture benefit from the spread in prices (while still respecting the user’s driving habits).

Having a look at the NPV of the project over the course of the year (cashflows relative to the baseline), we can see Octopus could make anywhere between £526 to £1015 per vehicle per year depending on market exposure, this also excludes the portfolio benefit Octopus could get from this additional flexibility which is likely to be material. We have also excluded the hardware costs of the charger.

A V2G blueprint for the future?

It's exciting to see a domestic supplier leading the way with V2G. It's been on the cards in theory for a while so it's great to see some moves being made in practice. It will be really interesting to see how this scheme develops, how quickly it scales and what hurdles they will inevitably face. At Gridcog, we firmly believe in flex and decentralisation of it; this scheme captures that spirit very well. Get in touch with one of the team if you have any questions on this topic, or are looking to model your EV fleet in Gridcog.

Take a look at our video on this topic below: