Zonal pricing, capacity markets, and the electricity market shakeup

The transition to low-carbon generation is driving a massive shift in electricity market design and fundamentals. We see this represented by the regular toppling of renewables records and a growing prevalence of volatile - and often negative - wholesale market pricing.

These dynamics bring into sharp focus the question of whether our electricity markets are fit for purpose. Crucially, do they provide the market (and therefore developers and customers) the right signals to invest in the assets the grid needs the most, in the places that they are most needed?

In this deep dive we’re going to take a look at market reforms in GB and Australia, with a focus on two key areas: locational pricing and capacity markets.

Locational pricing

In wholesale energy markets pricing can either be national, zonal or nodal.

The GB market currently has a national electricity price, meaning that the wholesale value of electricity is the same across the market in every settlement period, even if transmission constraints force the NESO control room to turn off wind in Scotland and turn on a gas peaker or Combined Cycle Gas Turbine (CCGT) in the South of England.

This is very different to a market like Australia’s NEM where pricing is zonal, meaning that the wholesale cost of electricity varies by pricing zone (the zones more or less align to state boundaries). In addition to zonal pricing the NEM also makes use of marginal loss factors, which offer further locational price signals as generation moves further from centres of demand.

Finally, markets like ERCOT and New Zealand are nodal markets with New Zealand having 226 Grid Exit Points (or pricing nodes) where Suppliers can buy and sell electricity, with these prices changing every five minutes.

The UK’s much anticipated REMA review was published last Thursday, 10th July 2025, with the biggest news being the government’s rejection of zonal pricing proposals. The government has instead opted to continue with a single national wholesale electricity market. In the update the government committed to implementing a Strategic Spatial Energy Plan by 2026 and will launch a review of Transmission Network Use of System (TNUoS) charges to provide some locational signals for investment.

Although zonal pricing dominated the headlines, REMA also covered other topics and the latest update covered targeted reforms to improve efficiency and flexibility. There are a number of proposals within this that could be game changers for flexibility in particular at the distribution scale including:

- Shortening settlement periods from 30 minutes to either 15 or 5 minutes

- Lowering the threshold for Balancing Mechanism participation for smaller assets

- Aligning BM gate closure with wholesale market trading windows.

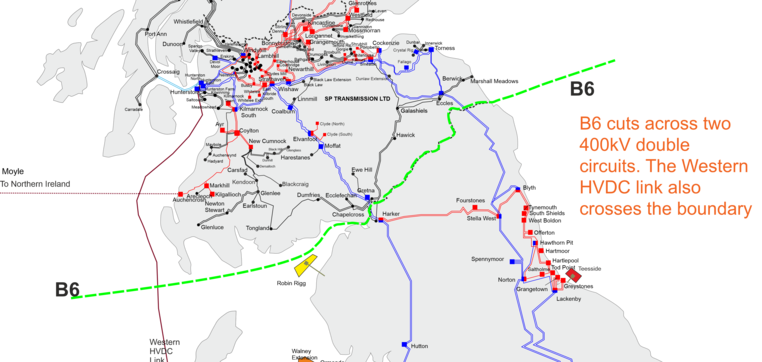

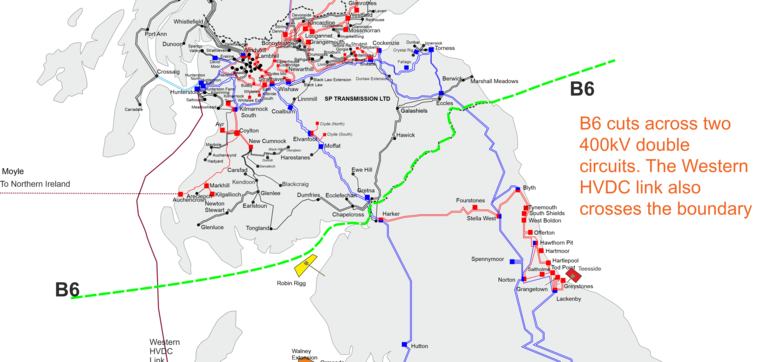

Arguably, zonal pricing supports a much more efficient energy system with much stronger incentives to co-locate load and generation. In NESO’s annual balancing report, published June 2025, they reported that £2.7bn was spent balancing the grid in the last fiscal year, with a very large portion of this cost the result of curtailing Scottish wind generation. This is because one of the biggest transmission constraints in GB lies across the B6 boundary point between England and Scotland.

Will zonal pricing fix grid inefficiencies?

A shift to zonal pricing would more directly pass these price signals through to consumers and developers and create a more price reflective electricity system.

However, there is fair criticism and confusion from the industry, in particular about how existing Contract for Difference (CfD) and subsidy measures will be grandfathered. This is a very delicate topic because if it’s done poorly could mean that new developments (and important investment into the energy transition) are paused or postponed due to investor uncertainty.

Meanwhile, Australia is also reviewing locational pricing signals as part of the Nelson Review. Although Australia already has zonal pricing this review is exploring whether sharper pricing signals are needed, citing inefficient congestion pricing at the moment.

Could this include a shift to real time locational marginal pricing, similar to the New Zealand model? This would more accurately reflect real time transmission costs, enabling more efficient dispatch, and sending investment signals to build assets where they are needed the most.

It’s interesting and timely that both markets are considering these reforms, as always with whatever option is adopted there will be critique and the devil will be in the detail as to how effective they will be.

Reforming capacity markets for a low-carbon future

Many energy markets have capacity markets or subsidies to incentivise investment in energy assets, with the primary goal of ensuring security of supply.

The GB market has had a Capacity Market since 2014 and one of the biggest criticisms of it is that by design it favours carbon intensive generators such as CCGTs and coal fired power plants (before they were all decommissioned).

This is because the portion of the capacity market payment generators receive is driven by the clearing price multiplied by a de-rating factor, with assets able to run for longer receiving a more favourable de-rating factor.

Introduction to Capacity Markets

REMA is also reviewing Capacity Market arrangements with potential for changes in market design to more directly reward low carbon generation. This could be via bid multipliers for low carbon generation, flexibility targets or minimum bid volumes to be secured from different generation types.

Australia’s Capacity Investment Scheme (CIS), a Government revenue support scheme for renewable generation and storage assets, is ending in 2027. As part of the Nelson Review they’re also exploring long-term replacement options including a firmed capacity market credit to incentivise low carbon generation and longer duration storage.

Modelling Capacity Markets in Gridcog

What’s next for GB and Australian electricity markets?

Although both the GB and Australian markets are fundamentally different, it is interesting to see the parallels between the REMA and Nelson Reviews. At Gridcog, we’ll be keeping a close eye on the outcome of these reviews and are ready to help our clients model the impacts of changes to market design in our software.

If you’re interested in learning more about this topic, we have plenty of other blogs and case studies to explore. If you want to discuss how Gridcog can model your energy projects, reach out to the team here.

This blog was first featured in our Thinking Energy newsletter, which you can subscribe to here.